Tech Insights

Memory Semiconductors in the ‘Memflation’ Era: Valuation Rerating Over Cycles

Jun 11, 2026

[Executive Summary]

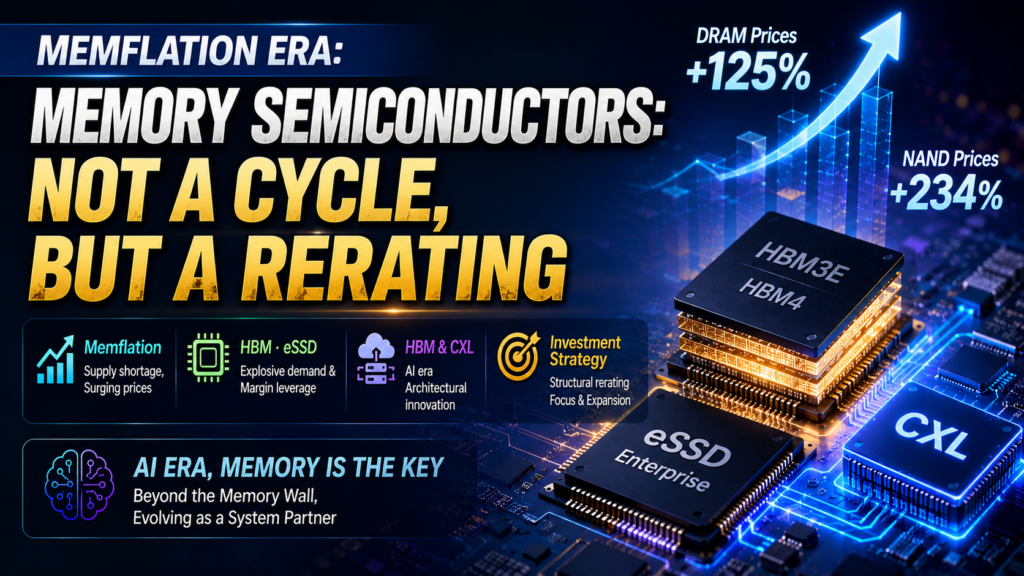

1. 2026 Core Market Keyword: ‘Memflation’

- Supply Shortages & Price Surges: Global semiconductor revenue is projected to surpass $1.3 trillion in 2026. Driven by explosive AI demand amid limited capacity expansions, the market has entered a ‘Memflation’ (Memory Inflation) phase, with DRAM prices surging by 125% and NAND flash by 234%. (Source: Gartner)

- Demand Bifurcation: As high pricing persists, non-AI consumer IT segments—such as PCs and smartphones—face ongoing risks of demand destruction and delayed purchases.

2. Product Trends & Margin Leverage

- DRAM: The concentration of fab capacity on HBM3E and HBM4 is cannibalizing the wafer capacity of conventional commodity DRAM (e.g., DDR5). This has triggered a chain reaction of supply shortages, supporting overall pricing and generating robust margin leverage.

- NAND: Growth is primarily fueled by enterprise SSDs (eSSD) for AI servers. In 2026, while AI accounts for 20% of NAND bit production, it is expected to drive mid-30% of total revenue, leading qualitative growth. Due to disciplined CapEx among major suppliers, tight supply-demand conditions are likely to persist through 2027.

3. Technology Paradigm Shift: Overcoming the ‘Memory Wall’

- Elevation to System Partners: With the surge in AI workloads exposing power and bandwidth limitations—known as the ‘Memory Wall’—memory has emerged as the critical bottleneck and key differentiator for AI performance.

- The Leap of HBM and CXL: Demand for HBM is soaring due to Cloud Service Providers (CSPs) developing proprietary AI chips (ASICs). Concurrently, the adoption of CXL (Compute Express Link)-based memory pooling is reshaping data center architectures. Consequently, memory manufacturers are evolving from mere component suppliers into ‘system co-design partners.’

4. Investment Strategy & Risk Management

- Valuation Framework Shift: Investors should transition away from traditional anxieties regarding short-term “cycle peaks.” Instead, the market warrants a “Structural Rerating” approach, driven by an elevated, baseline earning power from high-value products, justifying premium multiples compared to historical peaks.

- Portfolio Focus & Expansion:

- Concentrate on a select few top-tier memory makers with dominant technology and market leadership.

- Expand investments into critical material, component, and equipment supply chains related to advanced packaging (e.g., hybrid bonding, TSV)

- Selectively target beneficiaries of CXL and next-generation architectures.

- Risk Factors: Key risks requiring close monitoring and conservative leverage management include specs reduction (weakening demand) in non-AI downstream industries, US-China technological hegemony and regulatory risks, and shifting terms in Long-Term Supply Agreements (LSA).